Teaching Kids Money: An Age-by-Age Guide (3 to 18)

Age-Appropriate Money Lessons: From Toddlers to Teens

- Quick Answer: Teaching Kids Money

- What You’ll Learn About Teaching Kids Money:

- Why Financial Literacy Matters

- The Parent Mindset: You Don’t Need to Be an Expert

- 4 Core Principles for Success

- Teaching Kids Money by Age: The Complete Roadmap

- Ages 3-5: Teaching Kids Money Through Play

- Key Concept for Teaching Kids Money at This Age

- 3 Actionable Steps for Teaching Kids Money Ages 3-5

- Ages 6-8: Teaching Kids Money Management Hands-On

- Key Concepts for Teaching Kids Money at This Stage

- 3 Actionable Steps for Teaching Kids Money Ages 6-8

- Ages 9-12: Teaching Kids Money Budget Basics

- Key Concepts for Teaching Kids Money Planning

- Understanding Budget Development for Teaching Kids Money

- 3 Actionable Steps for Teaching Kids Money Ages 9-12

- Why the “Jar System” Works

- 2. Involving Them in Family Discussions

- 3. Decoding Marketing & Ads

- Ages 13-15: Teaching Kids Money Growth Concepts

- Key Concepts for Teaching Kids Money at Teen Stage

- Ages 13-15: Growth Concepts & Real Responsibility

- 3 Actionable Steps for Ages 13-15

- Ages 16-18: Financial Independence & Adult Skills

- 3 Actionable Steps for Ages 16-18

- Practical Tools

- Authoritative Online Resources

- Teaching Kids Money: Quick Reference Chart

- FAQ: Frequently Asked Questions

- What is the recommended allowance by age?

- What if my child wastes all their allowance immediately?

- How do I teach budgeting to a 7-year-old?

- Should I pay my child for chores or give free allowance?

- At what age should kids get their first debit card?

- When is the best time to start teaching kids about money?

- How do I explain “we can’t afford it” without creating anxiety?

- Conclusion: Your Roadmap

- Key Takeaways

- Your First Step

Teaching kids money skills transforms financial futures. In fact, teaching kids money doesn’t have to feel overwhelming for parents. However, most families struggle with these conversations. Moreover, teaching kids money can become one of the most empowering gifts you offer your children.

Furthermore, teaching kids money through this comprehensive guide provides a practical roadmap. Consequently, you’ll master this skill with simple, actionable steps for every age. Additionally, you’ll discover age-appropriate financial activities that make it engaging and fun.

Quick Answer: Teaching Kids Money

Teaching kids money is an age-based system that introduces financial concepts through hands-on activities from coin recognition at age 3 to investing basics at 18. This method works for any parent committed to 5-10 minutes weekly, using simple tools like savings jars, allowances, and real-world conversations to build lifelong money skills.

What You’ll Learn About Teaching Kids Money:

- Teaching kids money lessons for ages 3-18

- Practical activities at each stage

- Expert tips for stress-free

Why Financial Literacy Matters

Before diving into strategies, understand this critical fact: Money habits form by age 7. This means starting early gives your children a powerful lifelong advantage. Financial literacy isn’t just about being rich; it impacts academic performance, reduces future stress, and sets the foundation for a successful independent life.

The Parent Mindset: You Don’t Need to Be an Expert

Here is the truth: You don’t need a degree in finance to teach your kids about money.

Focus on Habits, Not Math: It is about building healthy behaviors (like waiting to buy something) rather than complex theory.

Consistency > Perfection: You don’t need to get it right every time. Small, regular conversations create a lasting impact.

4 Core Principles for Success

1. Keep It Positive & Age-Appropriate Frame money as a tool for achieving goals, not a source of worry.

Avoid: “We have no money.” (Creates anxiety).

Try: “We are choosing to save our money for [Goal] instead.” (Empowers them).

2. Use Everyday Moments You don’t need a classroom. The world is your school.

Grocery Stores: Perfect for comparing prices.

Gas Stations: Good for discussing rising costs.

Family Outings: Ideal for budgeting (“We have $20 for snacks, how should we spend it?”).

3. Focus on “Empowerment” Language Change how you say “No.” Instead of saying “We can’t afford that,” try this script:

“That is not in our budget right now, but let’s make a plan to save for it.” This shifts the focus from restriction (I can’t) to empowerment (I can plan).

4. Be Honest About Your Mistakes Share small past mistakes to show you are human.

Example: “I once bought a gadget I didn’t need and regretted it later because it broke in a week.” This makes you relatable and teaches them that making mistakes is part of the learning process.

Teaching Kids Money by Age: The Complete Roadmap

Financial education evolves as your child grows. Below is your complete guide for managing money lessons at every stage, from toddlerhood to the teen years. Each section includes research-backed strategies designed for that specific developmental stage.

Ages 3-5: Teaching Kids Money Through Play

Key Concept for Teaching Kids Money at This Age

When teaching kids money skills at age 3-5, focus on concrete concepts. Moreover, hands-on learning works best for preschoolers. Furthermore, teaching kids money at this early stage sets the foundation for future financial literacy.

3 Actionable Steps for Teaching Kids Money Ages 3-5

1. Use a Clear Jar for Teaching Kids Money Saving

A clear jar is essential when teaching kids money concepts visually. In contrast to traditional piggy banks, clear containers show accumulation. Therefore, teaching kids money through visible savings makes the abstract idea real.

How to implement teaching kids money with jars:

- First, choose a plastic jar for safety

- Next, let them drop coins in after good behavior

- Then, count together weekly

- Finally, celebrate when the jar gets fuller

Additionally, this simple tool makes saving tangible for young minds while teaching kids money fundamentals.

2. Play “Store” for Teaching Kids Money Exchange

This is highly effective for teaching kids money transactions. Moreover, put price tags on toys and provide play money. Consequently, teaching kids money through play helps children understand exchange concepts.

How to implement teaching kids money through play:

- Use play money or create your own

- Start with simple prices ($1, $2, $5)

- Let them be both customer and cashier

- Make teaching kids money fun, not a test

Furthermore, role-playing builds confidence with money interactions while teaching kids money skills.

3. Teaching Kids Money: Needs vs. Wants

Use simple scripts during everyday activities when teaching kids money priorities:

“We need to buy apples and bread for our meals. Those cookies are something we want. Since we’ve been good with our budget this week, let’s get them as a special treat.”

Just like offering choices helps when a Toddler Won’t Eat, offering financial choices empowers them.

💡 Pro Tip for Teaching Kids Money: Make a game of identifying needs vs. wants during grocery shopping! Moreover, this builds critical thinking skills early while teaching kids money awareness.

Real-Life Scenario (Age 5): The “Grocery Store Waiting Game”

The Situation: Your 5-year-old sees a candy bar at the checkout and screams, “I want it!”

Old Way: “No, we can’t afford that.” (Creates anxiety).

New Way: “That looks yummy! Is it on our list today? No? Let’s put it on your ‘Wish List’ for next time, or you can use your ‘Spend Jar’ money when we get home.”

The Lesson: Impulse control and planning.

Ages 6-8: Teaching Kids Money Management Hands-On

Key Concepts for Teaching Kids Money at This Stage

At this stage, teaching kids money involves more complex ideas. Additionally, children can now grasp the work-earning connection. Therefore, teaching kids money at ages 6-8 introduces more responsibility and independence.

3 Actionable Steps for Teaching Kids Money Ages 6-8

1. Start an Allowance System for Teaching Kids Money

This is one of the best methods for teaching kids money responsibility. Moreover, tie allowance to simple household chores when teaching kids money work ethics. As a result, teaching kids money through allowances demonstrates the fundamental link between work and earning.

Recommended allowance formula for teaching kids money:

- $0.50 to $1.00 per year of age, per week

- Example: $3-$6 per week for a 6-year-old

- Adjust based on your family budget

Expert Tip for Teaching Kids Money: Consider having some chores be unpaid “family contributions.” Therefore, teaching kids money includes community responsibility. Furthermore, this balanced approach follows expert recommendations.

2. Open Their First Savings Account When Teaching Kids Money

Teaching kids money management becomes more impactful with a real bank account. Moreover, visiting a bank makes teaching kids money feel important. Additionally, teaching kids money through financial institutions introduces positive banking relationships.

Steps for teaching kids money through bank accounts:

- First, research banks offering no-fee child accounts

- Then, bring required documents (birth certificate, Social Security card)

- Next, let your child sign paperwork (with help)

- Additionally, set up mobile banking for teaching kids money tracking

- Finally, make deposits a special ritual when teaching kids money habits

3. Teaching Kids Money Through Real Purchases

The physical act of exchanging money is powerful for teaching kids money transactions. Therefore, give them opportunities to use cash. Moreover, handling real purchases builds confidence when teaching kids money skills.

How to implement teaching kids money with purchases:

- Start with purchases under $10

- Help them count money before checkout

- Let them handle the transaction alone

- Discuss the experience afterward

Real-Life Scenario (Age 7): The “Commission” Switch

The Situation: Your child wants a $20 Lego set but has $0.

The Strategy: Instead of buying it for them, switch from “Allowance” (money for existing) to “Commission” (money for work).

The Script: “You have $5 in your jar. You need $15 more. I have 3 extra jobs (washing the car, raking leaves) that pay $5 each. If you do them this weekend, you can buy the Lego on Sunday.”

The Lesson: Money comes from work, not magic.

Ages 9-12: Teaching Kids Money Budget Basics

Key Concepts for Teaching Kids Money Planning

Teaching kids money at this age introduces deliberate financial choices. Furthermore, tweens are developmentally ready for abstract thinking. Therefore, teaching kids money budgeting basics works perfectly now.

Understanding Budget Development for Teaching Kids Money

Moreover, this age group can understand delayed gratification when teaching kids money planning. Additionally, they can make plans for saving. Consequently, teaching kids money through budgeting tools becomes highly effective.

3 Actionable Steps for Teaching Kids Money Ages 9-12

1. Three-Jar System for Teaching Kids Money Allocation

This visual tool is essential for teaching kids money distribution. Furthermore, get three clear jars labeled “Save,” “Spend,” and “Give.” Then, teaching kids money percentages helps them decide jar allocation.

Recommended split for teaching kids money:

- Save: 30% (long-term goals)

- Spend: 50% (short-term wants)

- Give: 20% (charity or gifts)

Why the “Jar System” Works

This system is superior to a piggy bank because:

Visual Learning: They can literally see their money growing or shrinking.

Delayed Gratification: It forces them to pause and decide where the money goes.

Balanced Values: It encourages generosity (Give) while still allowing them to enjoy their money (Spend).

Proven Success: This method is widely recommended by financial experts for teaching allocation skills.

2. Involving Them in Family Discussions

Don’t make money a secret topic. Include your children in age-appropriate real-world decisions. This builds trust and practical skills.

Opportunities to involve them:

Planning the weekly meal budget.

Finding the best deal on a specific purchase (e.g., “Find the cheapest cereal”).

Comparing prices between different stores.

Helping plan the family vacation budget (e.g., choosing between two activities).

How to implement this:

Share Info: Give them the numbers (e.g., “We have $20 for snacks”).

Ask for Input: “What do you think we should buy?”

Explain: Walk them through why you made the final decision.

Celebrate: If their idea saved money, high-five them or let them keep the change!

3. Decoding Marketing & Ads

Critical thinking is your child’s best defense against overspending. When you see commercials on TV or online, use them as a “Pop Quiz.”

Ask these 4 questions:

“What feeling is this ad trying to sell you?” (Happiness? Popularity?)

“Do you think the toy really moves/flies like that in real life?”

“What are they NOT telling you?” (e.g., batteries not included).

“Is this a Need or a Want?”

The Result: This turns them from passive viewers into critical consumers who think before they buy.

💡 Pro Tip: Use YouTube ads as teaching moments. Since tweens spend significant time online, pause the video when an influencer promotes a product and analyze it together. This builds smart habits in the digital age.

Real-Life Scenario (Age 10): The “Robux” Dilemma

The Situation: Your 10-year-old spends all their monthly allowance on a video game skin in one day, then asks for more money for ice cream.

The Hard Part: You must say No.

The Script: “I know you’re frustrated. You chose to spend your budget on the game. That was your choice. Next month, you can plan differently. I’m not going to bail you out.”

The Lesson: Opportunity cost (If you buy A, you can’t buy B).

Ages 13-15: Teaching Kids Money Growth Concepts

Key Concepts for Teaching Kids Money at Teen Stage

Teaching kids money at this stage introduces abstract financial concepts. Specifically, teaching kids money now includes the power of time in growing wealth. Moreover, teaching kids money incorporates long-term financial planning.

Managing money requires the same maturity as managing technology. Read our guide on Phone-Free Teens: A 7-Day Plan to build responsibility.

Ages 13-15: Growth Concepts & Real Responsibility

Key Concepts: At this stage, teens are ready for abstract financial concepts. They can comprehend exponential growth (how money multiplies) and “opportunity cost” (what you lose when you choose one option over another). This is the perfect time to shift from “saving” to “wealth building.“

3 Actionable Steps for Ages 13-15

1. Encouraging Outside Earning (The First “Job”)

Shift the conversation from allowance to “earnings.” Encourage them to find work outside the house to understand the true value of labor.

Real-world earning ideas:

Babysitting for neighbors.

Dog walking or pet sitting.

Lawn mowing or yard work.

Tutoring younger students.

Selling crafts or digital art online (with supervision).

Why this matters: It builds entrepreneurial thinking, time management, and customer service skills that school doesn’t teach.

2. The Power of Compound Interest

This is often the most powerful “aha!” moment for teens. Explain it simply: “Your money earns its own money.”

The “Cost of Waiting” Example: Use a simple online calculator to show them this math:

Scenario A: Invest $100 today at 7% return = Grows to $760 in 30 years.

Scenario B: Wait 10 years to start = Grows to less than $400.

The Lesson: Time is their biggest financial advantage. Even small savings now have a massive impact later.

3. Debit Card Responsibility (Going Digital)

Cash is great, but the world is digital. Open a teen checking account to teach them how to manage invisible money.

The Basics to Master:

Tracking: Checking their balance via mobile app before buying.

Debit vs. Credit: Explaining that a debit card uses their money, while credit is borrowed money (debt).

Alerts: Setting up text notifications for every purchase.

Safety & Security:

Protecting PIN numbers (never sharing them with friends).

Recognizing Phishing Scams (fake emails/texts asking for info).

Practicing safe online shopping (only buying from trusted sites).

Ages 16-18: Financial Independence & Adult Skills

Key Concepts: At this stage, the focus shifts to adult responsibilities. The goal is to prepare your teen to manage finances confidently without you hovering over their shoulder. This includes understanding credit, debt, and the basics of investing.

Building Financial Independence: Teens in this age group need real-world practice to build autonomy. Introduce complex topics gradually so they can transition smoothly to independent financial management before they leave the nest.

3 Actionable Steps for Ages 16-18

1. Budgeting for Major Goals

Shift the focus from small purchases to significant financial milestones. Help them create a budget for:

Their first car.

A laptop for college.

Senior trip expenses.

Moving-out costs (deposit + first month’s rent).

How to create a “Big Goal” plan: Sit down together and map out:

Total cost: How much do they actually need?

Timeline: When do they need it?

Monthly savings: Divide the cost by the months remaining.

Tracking: Use a spreadsheet or a budgeting app to track progress.

2. Understanding Credit Scores

What affects their score:

Payment History (35%): Paying on time is the most important factor.

Credit Utilization (30%): How much of their limit they use.

Length of History (15%): How long they have had credit.

Why it matters: Explain that a bad score can stop them from renting an apartment, getting a car loan, or even getting certain jobs.

Action Step: Consider adding them as an “Authorized User” on your credit card. Explain the rules clearly, monitor usage together monthly, and require them to pay off their portion immediately. This builds their history safely.

3. Basic Investing Concepts

You don’t need to be a Wall Street expert to teach this. Focus on the simple logic of wealth growth.

Stock Market Basics:

Stocks: Owning small pieces (shares) of companies.

Risk vs. Reward: Higher potential returns come with higher risks.

Long-term: Investing is for money you won’t touch for 5+ years.

The “Diversification” Rule: Teach them “Don’t put all your eggs in one basket.” Explain how Index Funds or ETFs allow them to own a tiny piece of hundreds of companies at once, which is safer than betting on just one stock.

How to Start:

Use apps that allow fractional shares (investing as little as $5).

Encourage them to invest $25-$50 of their summer job money.

Practical Tools

You don’t have to do this alone when teaching kids money. Therefore, here are vetted resources. Additionally, these tools make it engaging and fun.

Authoritative Online Resources

Consumer Financial Protection Bureau (CFPB)

- “Money as You Grow” section

- Activities for kids of all ages

- Trusted government resource

National Endowment for Financial Education (NEFE)

- Free lesson plans by age

- Printable worksheets included

- Financial literacy standards

- Comprehensive guide with concepts

- Compound interest calculator

- Investment basics for teens

- SEC-backed resource

- Advanced tool for growth strategies

- Financial literacy research

- Educational standards and benchmarks

- Teacher and parent resources

- Evidence-based approach

- Interactive games and activities

- Lesson plans for all ages

- Real-world simulations

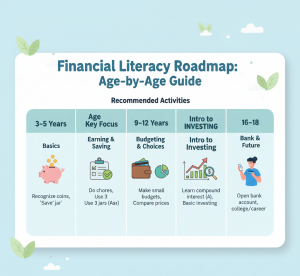

Teaching Kids Money: Quick Reference Chart

| AGE | KEY CONCEPT | BEST ACTIVITIES | PRIMARY GOAL |

|---|---|---|---|

| 3-5 | Money is for exchange | Clear jar savings, play store, needs vs wants | Make money concrete |

| 6-8 | Earning and saving | Allowance, bank account, small purchases | Connect work to earning |

| 9-12 | Budgeting basics | Three-jar system, family discussions, ad analysis | Teach money planning |

| 13-15 | Growth and earning power | Outside jobs, compound interest, debit cards | Understand money growth |

| 16-18 | Complex finances | Major budgets, credit basics, investing concepts | Prepare for independence |

FAQ: Frequently Asked Questions

What is the recommended allowance by age?

The most common formula is $0.50 to $1.00 per year of age, per week. Ages 5-7 receive $5-8 weekly, ages 8-10 get $8-12, ages 11-13 receive $10-15, and ages 14-17 get $15-30 weekly. Adjust based on your family budget and what expenses you expect them to cover.

What if my child wastes all their allowance immediately?

Let them experience the natural consequence without bailing them out. Use it as a teaching moment: “I know you’re frustrated. You chose to spend your budget on . That was your choice. Next month, you can plan differently.” Small financial mistakes now prevent bigger ones later

How do I teach budgeting to a 7-year-old?

Start with the three-jar system: “Save” (30%), “Spend” (50%), and “Give” (20%). Use clear jars so they see money accumulate. Give them small purchasing decisions at the grocery store ($5-10 budget) and involve them in comparing prices. Make it hands-on and visual rather than abstract.

Should I pay my child for chores or give free allowance?

Experts recommend a hybrid approach: keep basic tasks like making beds unpaid as “family contributions,” but offer extra chores (washing car, yard work) for commission-based earnings. This teaches both community responsibility and the work-earning connection without making everything transactional.

At what age should kids get their first debit card?

Most experts recommend ages 13-15 for introducing debit card responsibility. Open a teen checking account with spending alerts and teach them to check balances before purchases. This prepares them for managing digital money while you can still supervise transactions.

When is the best time to start teaching kids about money?

Start as early as age 3 with simple coin recognition and play activities. Research from Cambridge University shows money habits form by age 7, making early childhood the critical window. Even toddlers can learn that money is exchanged for things they want.

How do I explain “we can’t afford it” without creating anxiety?

Replace “We can’t afford that” with empowerment language: “That’s not in our budget right now, but let’s make a plan to save for it” . This shifts from restriction (can’t) to planning (can with preparation). Frame budgeting as a tool to get what they want, not punishment.

Conclusion: Your Roadmap

Teaching kids money management is an ongoing journey, not a one-time lecture. Moreover, if you start early and be consistent transforms a potentially stressful topic. Consequently, it becomes a source of confidence and empowerment for your children.

Key Takeaways

- Start early – Begin at age 3 with simple, concrete concepts

- Stay age-appropriate – Tailor lessons to your child’s developmental stage

- Be consistent – Use tools like allowances, savings jars, and regular conversations

- Use real-world moments – Everyday decisions are perfect teaching opportunities

- Model healthy habits – Your relationship with money teaches more than your words

- Allow small mistakes – Low-stakes errors teach valuable lessons

- Focus on empowerment – Frame financial literacy as a superpower, not a restriction

Your First Step

Ready to begin your journey of teaching kids money skills? Therefore, choose just one action from this guide to try this week:

- Ages 3-5: Set up a clear savings jar

- Ages 6-8: Open their first bank account

- Ages 9-12: Start the three-jar budgeting system

- Ages 13-15: Calculate compound interest together

- Ages 16-18: Create a budget for their major goal

Remember: teaching kids money skills doesn’t require perfection. Instead, teaching kids money requires consistency, patience, and the willingness to start today. Moreover, teaching kids money means your child’s financial confidence begins with one small conversation, one saved dollar, one smart decision at a time.

What will your first step be ? Share your plan in the comments below!